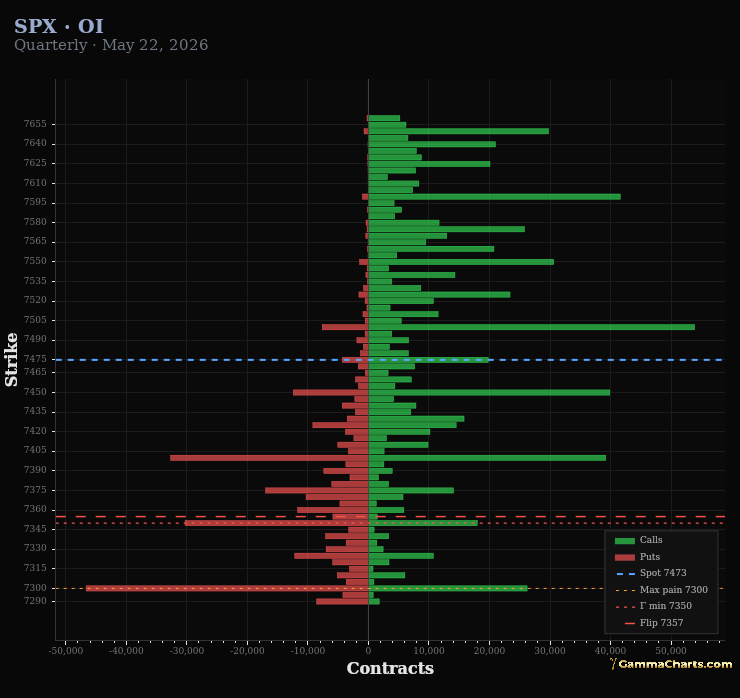

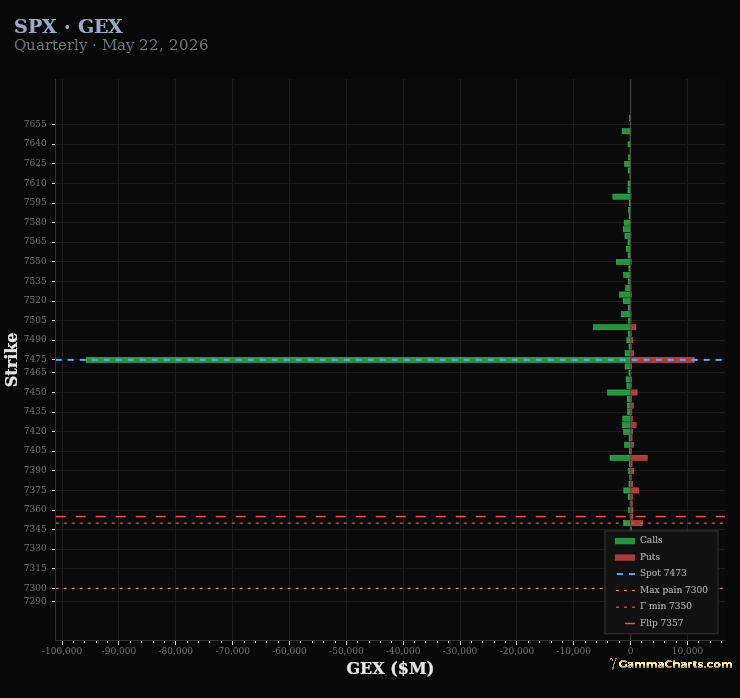

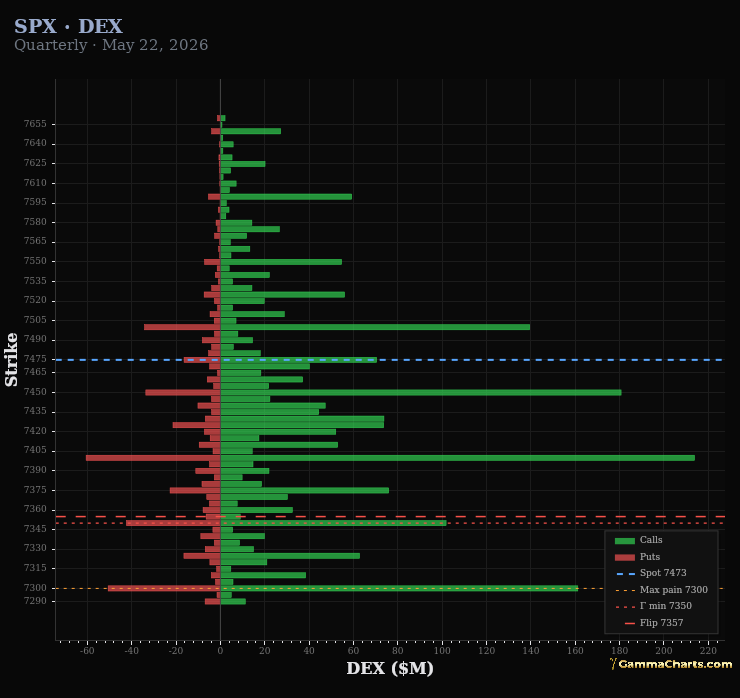

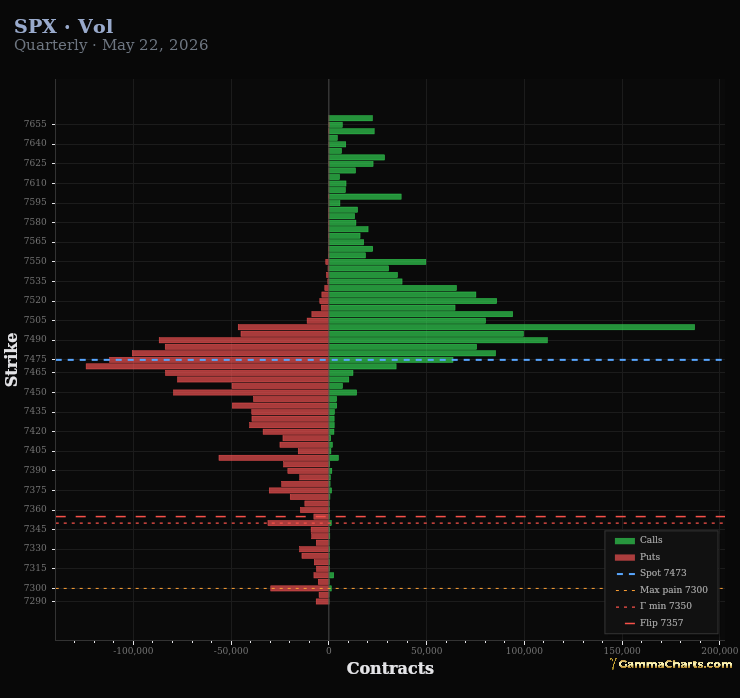

Options Curve SPX

@gammacharts

Assumes a uniform 1-point IV shift across all strikes.

Drift shown per single calendar day; multi-day gaps scale linearly.

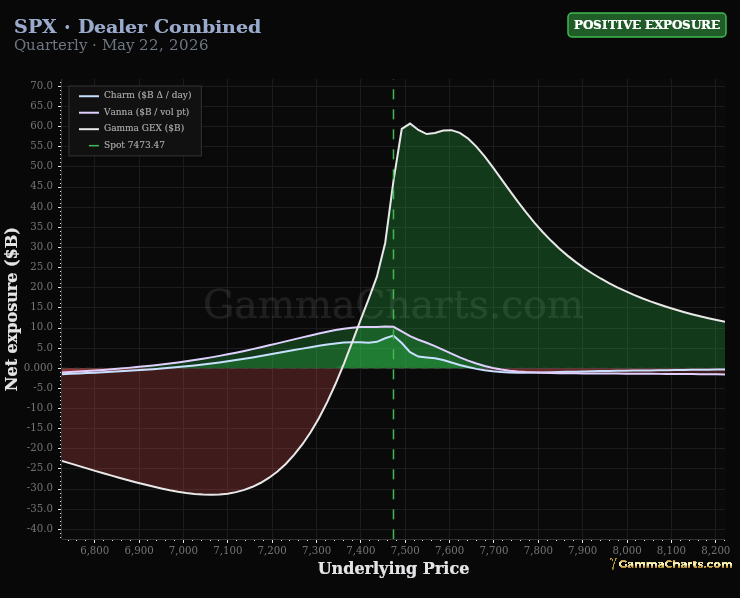

All three series in $B; y-axis units differ by greek (see legend).

What it shows

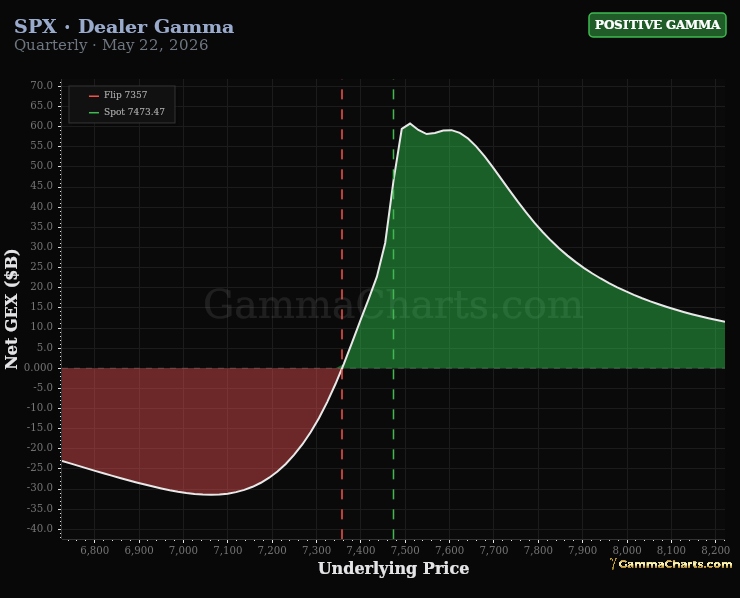

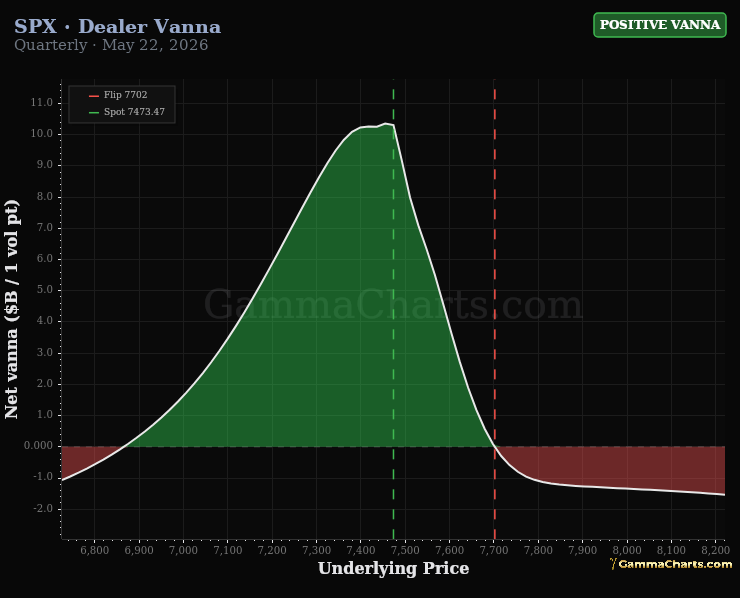

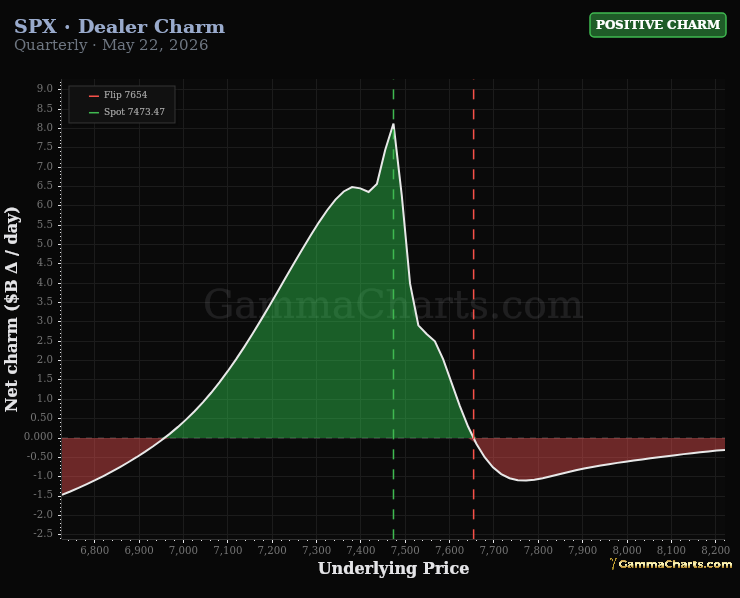

Estimated dealer Greek exposure by strike: where the book flips sign and how much hedging flow each level implies. Assumptions are noted under each tab.

The tabs

- Gamma — S-curve of net gamma; zero-cross is the gamma flip (regime change level).

- Vanna — Delta sensitivity to a parallel 1-point IV shift across strikes.

- Charm — Delta drift per calendar day with spot and vol held flat.

- Combined — All three in $B; y-axis units differ by Greek (see legend).

How to use it

- Mark the flip strike on Gamma first — price above/below defines long- vs short-gamma hedging bias.

- Use Vanna/Charm when vol or time decay is the driver (event weeks, 0DTE-heavy sessions).

- Compare to Chain GEX by strike for the same tier — profiles should tell a consistent story.