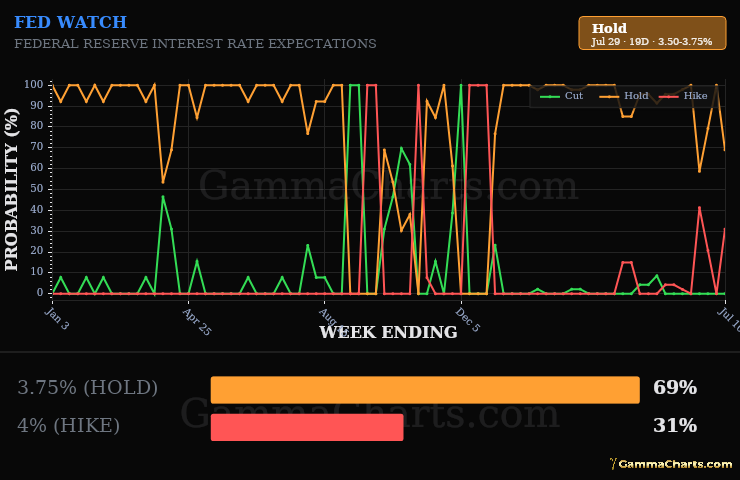

Fed Watch

Fed watch

Fed Watch translates 30-day Fed Funds futures pricing into probabilities for the next FOMC decision. The futures contract settles on the average effective federal funds rate for the month, so the market price embeds expectations for both the pre-meeting days and the post-decision days in that month.

This chart applies the standard day-weighting adjustment: it solves for the implied post-meeting rate, then spreads probability across 25 bp target bands. The top panel tracks weekly shifts in cut/hold/hike odds; the bottom panel shows today's full rate-band breakdown.

How to read it

- Top — weekly trend — Green is cut, orange is hold, red is hike. Each point uses that week's last futures close.

- Bottom — rate bands — Horizontal bars are possible target ranges after the next meeting. The highlighted band is today's target; bar length is implied probability.

- Badge — Dominant outcome today, days to the next FOMC, and the current target band.