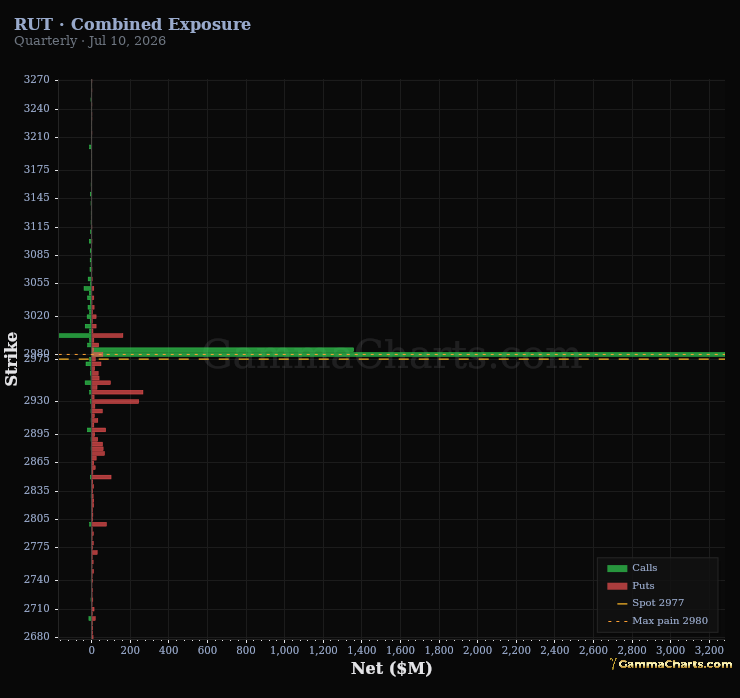

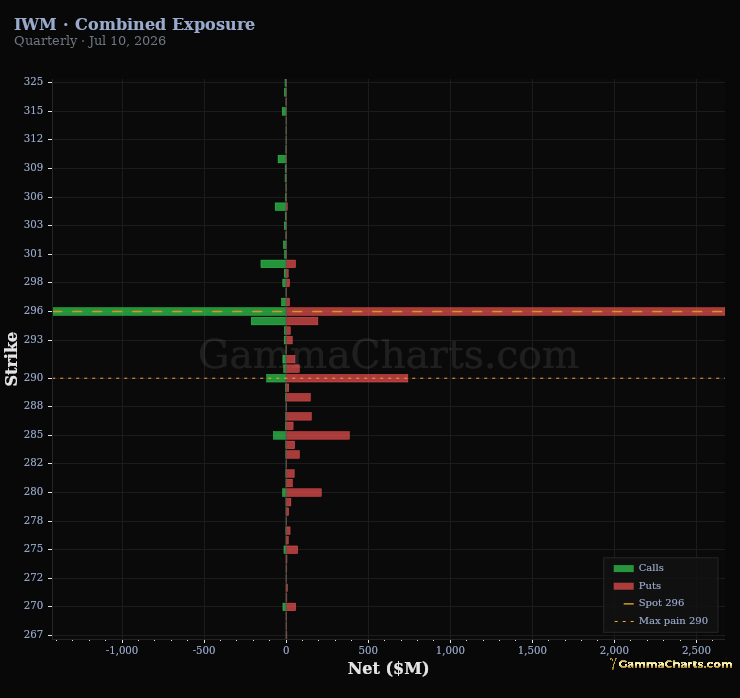

Greek Exposure

Greek Exposure

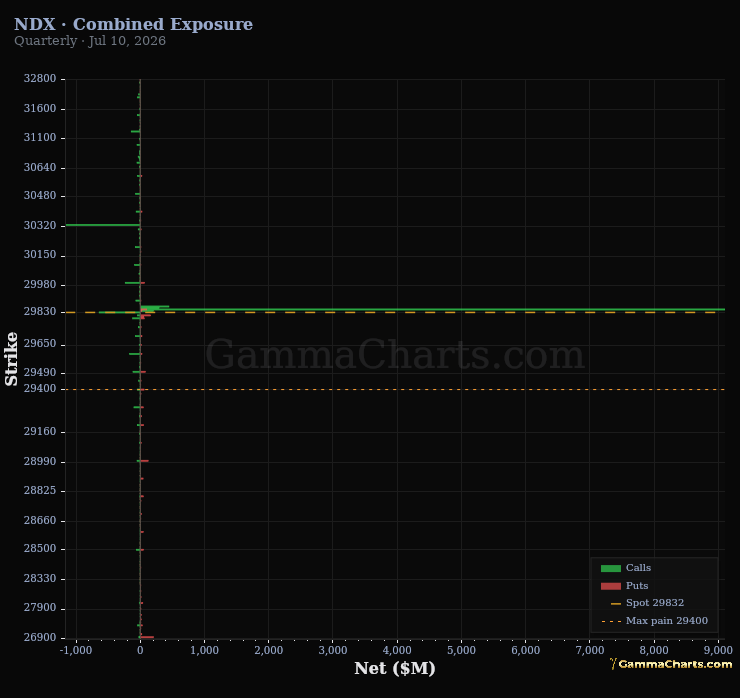

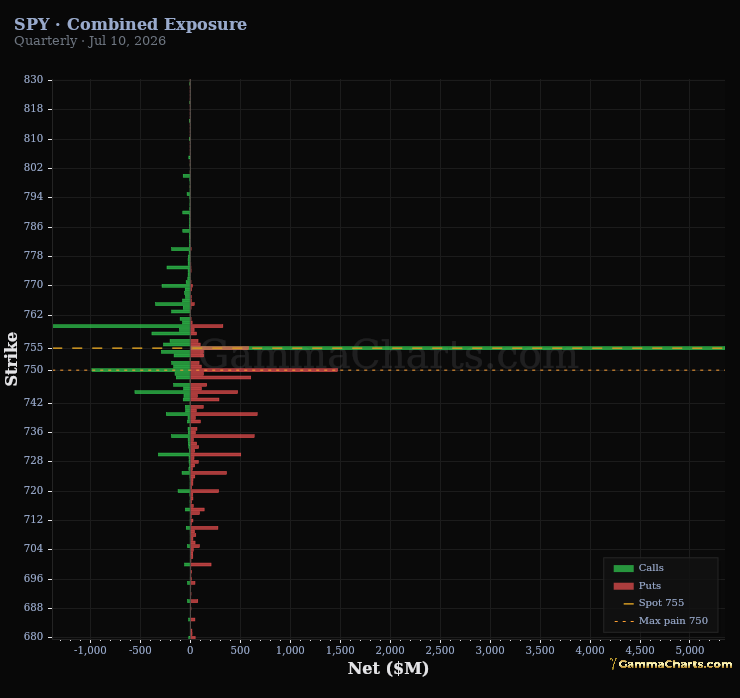

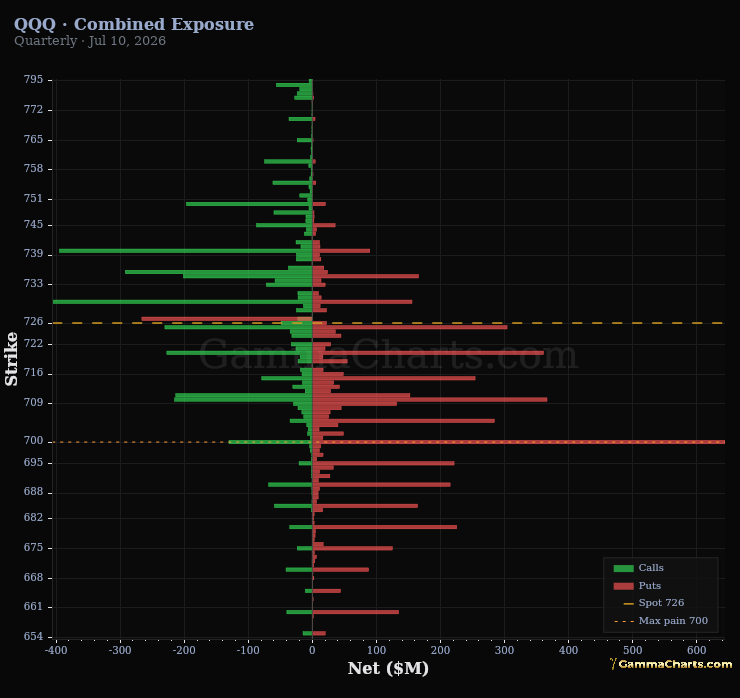

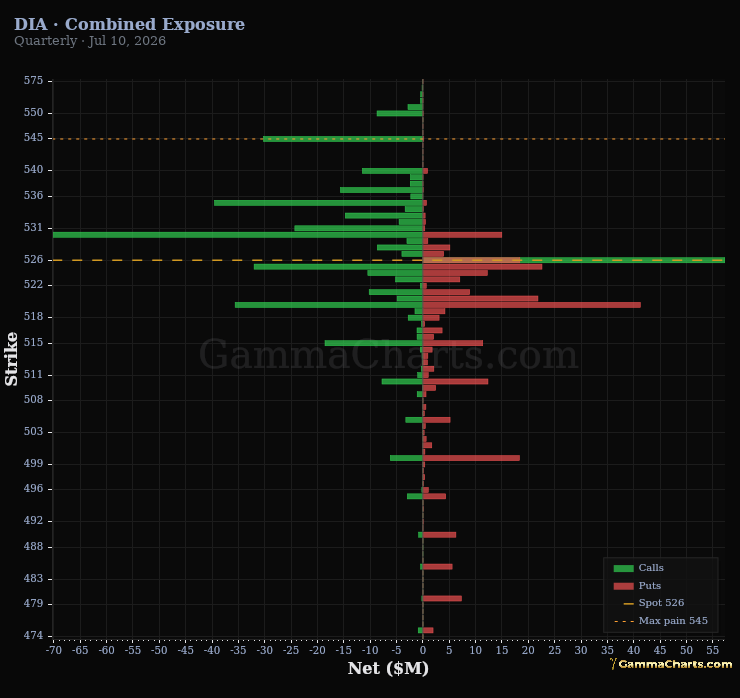

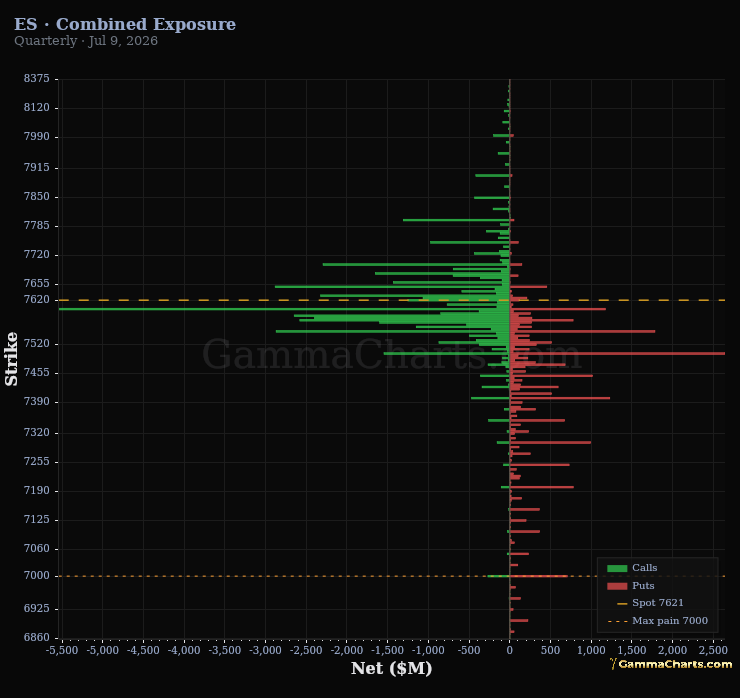

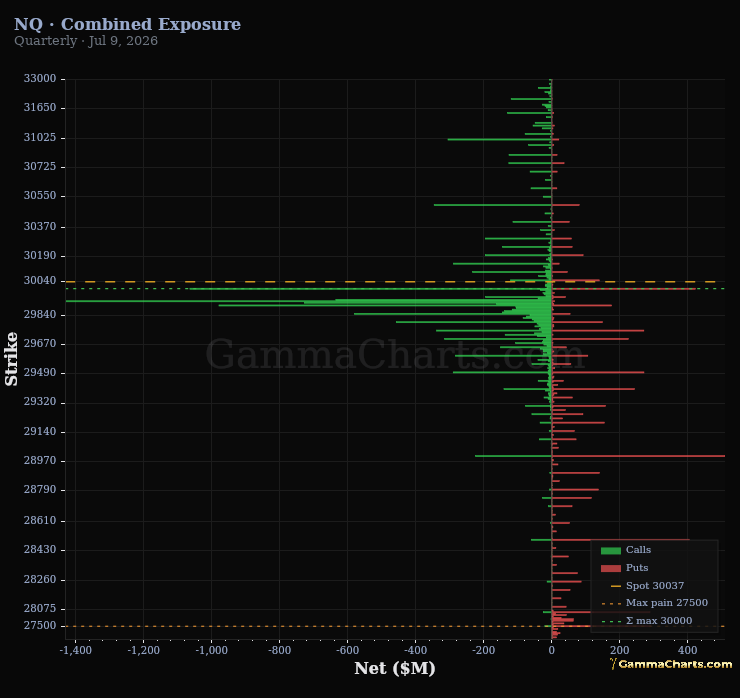

Market makers are assumed to be delta-neutral — they hedge their directional exposure continuously. This chart shows the estimated hedging requirements that flow from that assumption, broken down by greek and expiration.

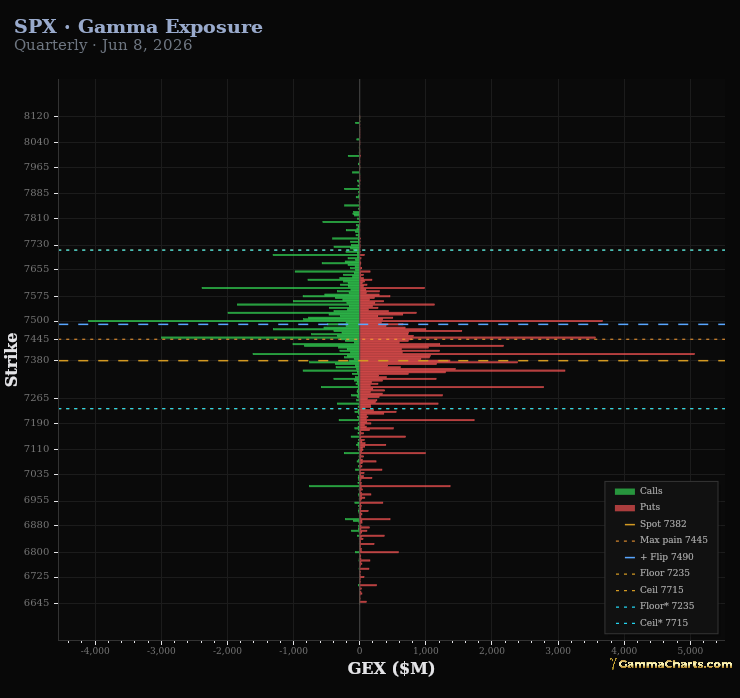

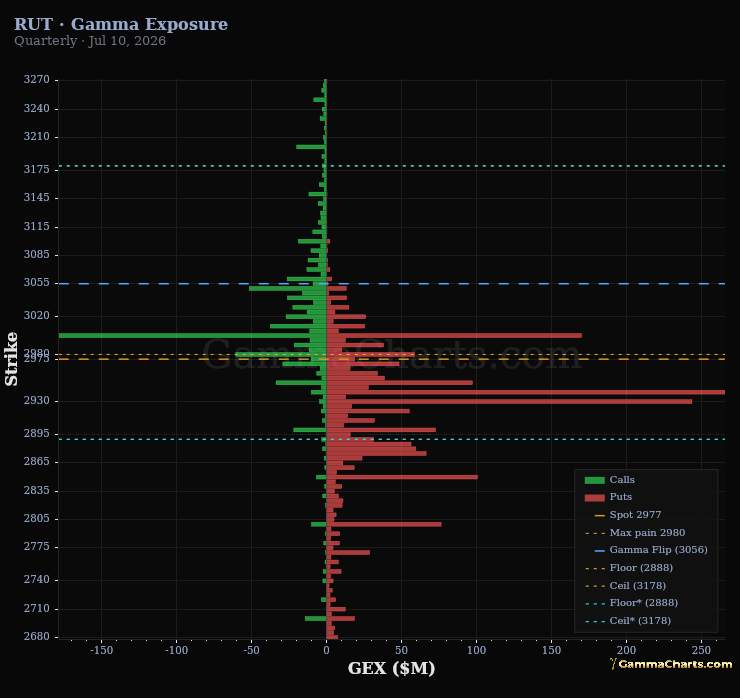

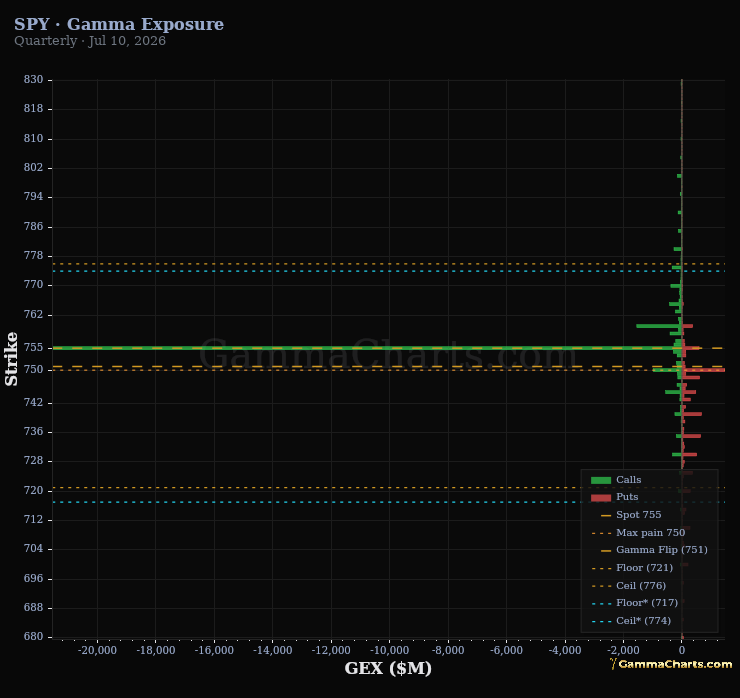

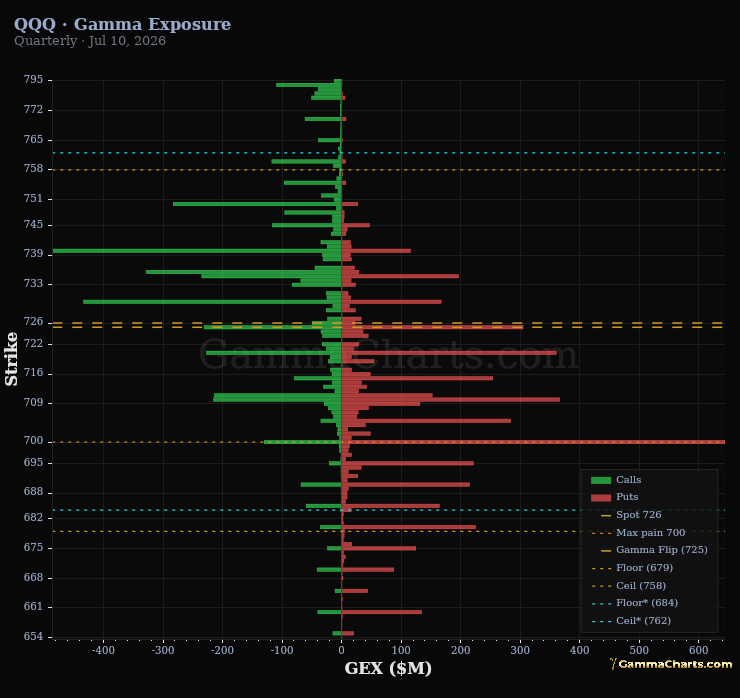

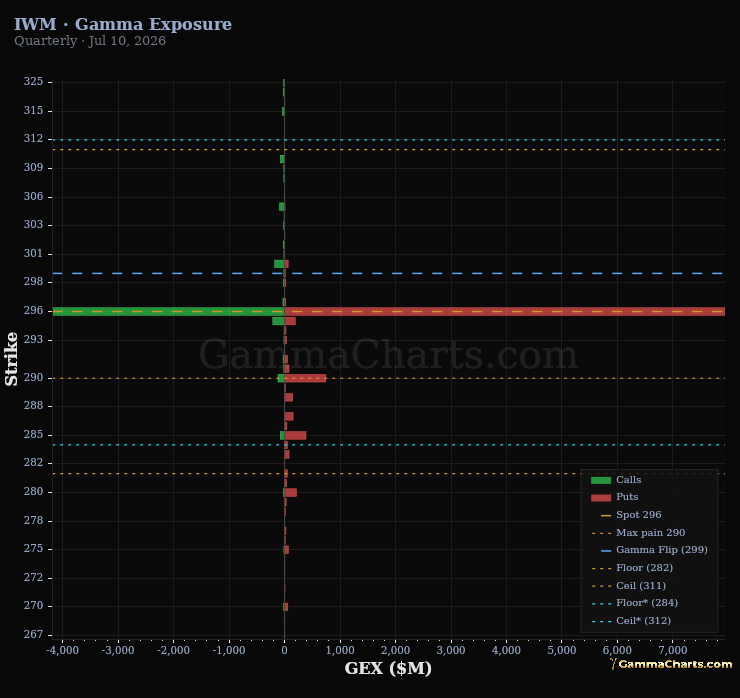

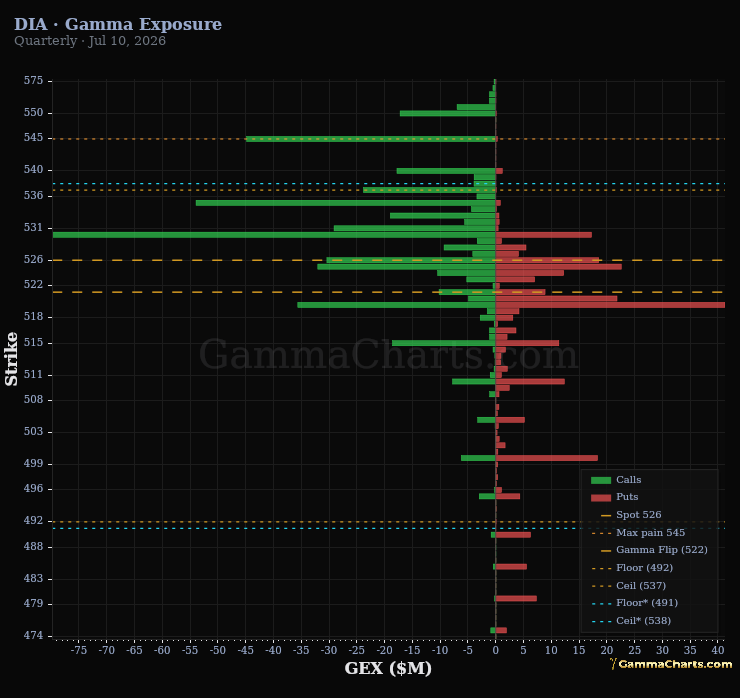

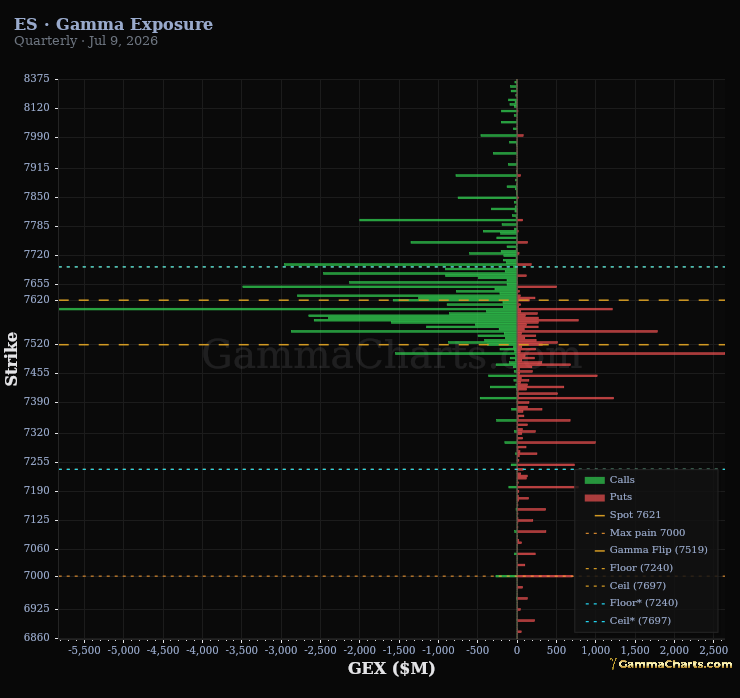

Gamma

Gamma is how much dealers must buy or sell spot as price moves. Positive gamma means they sell into rallies and buy dips; negative gamma amplifies moves.

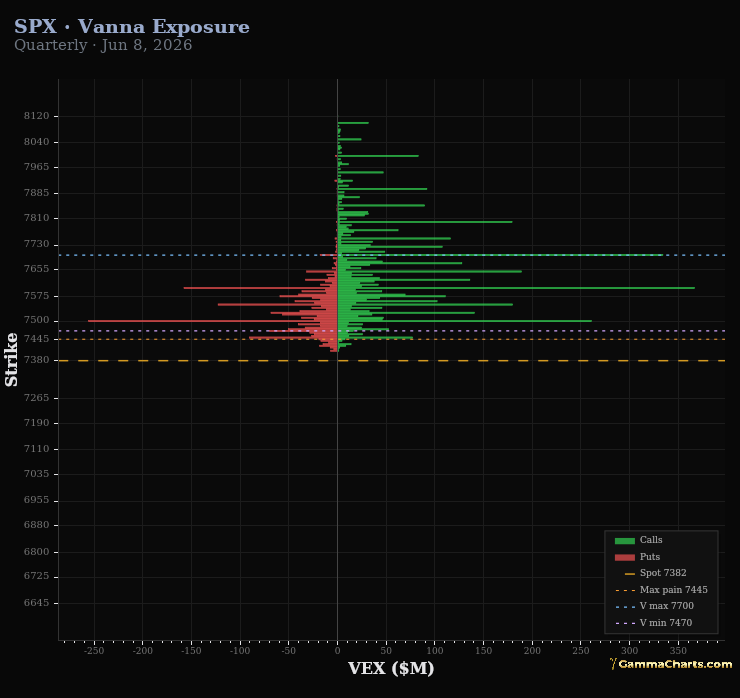

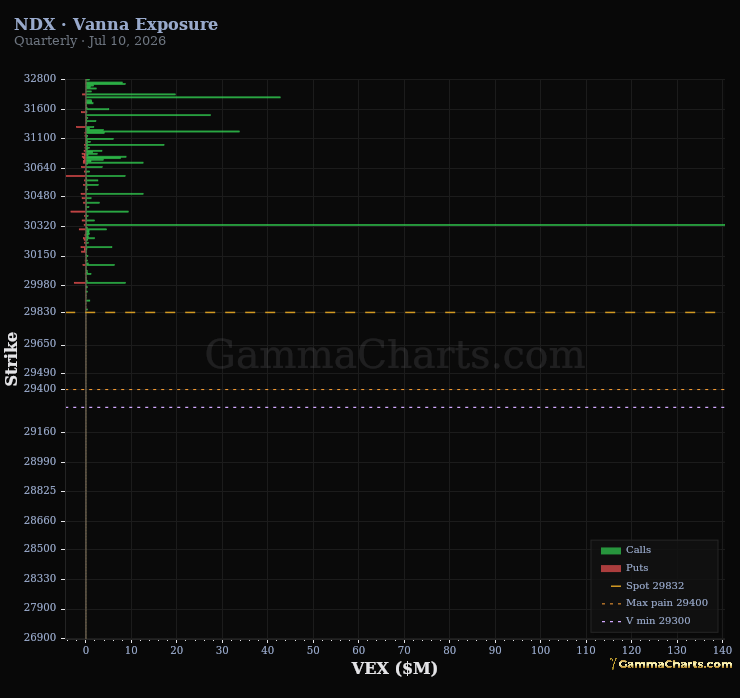

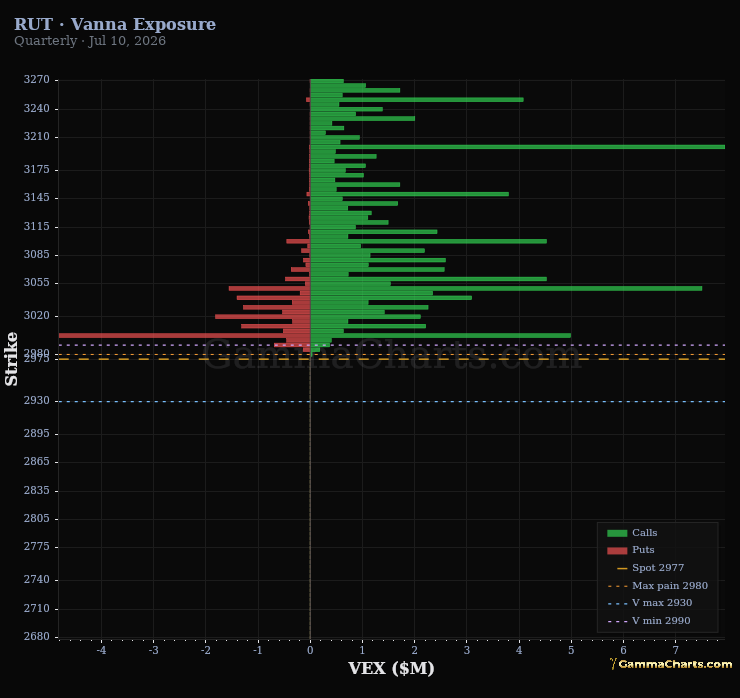

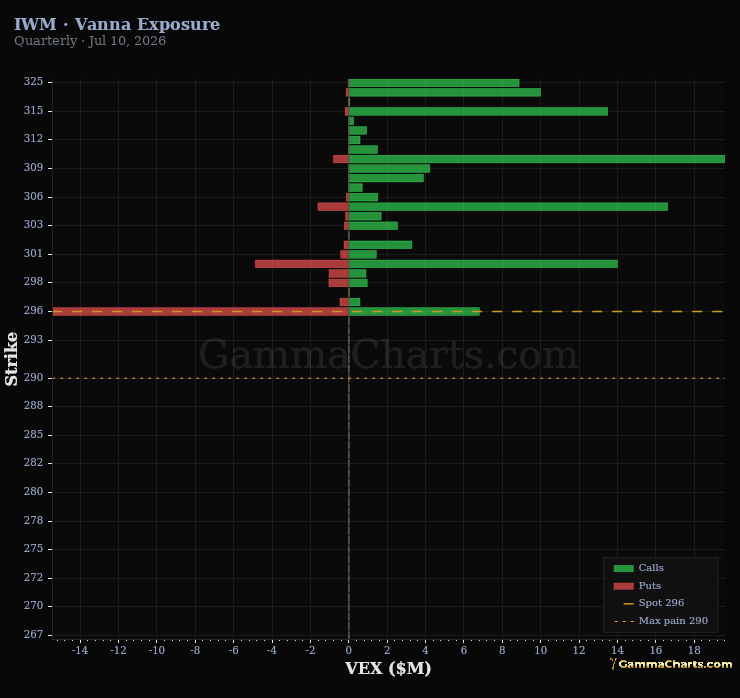

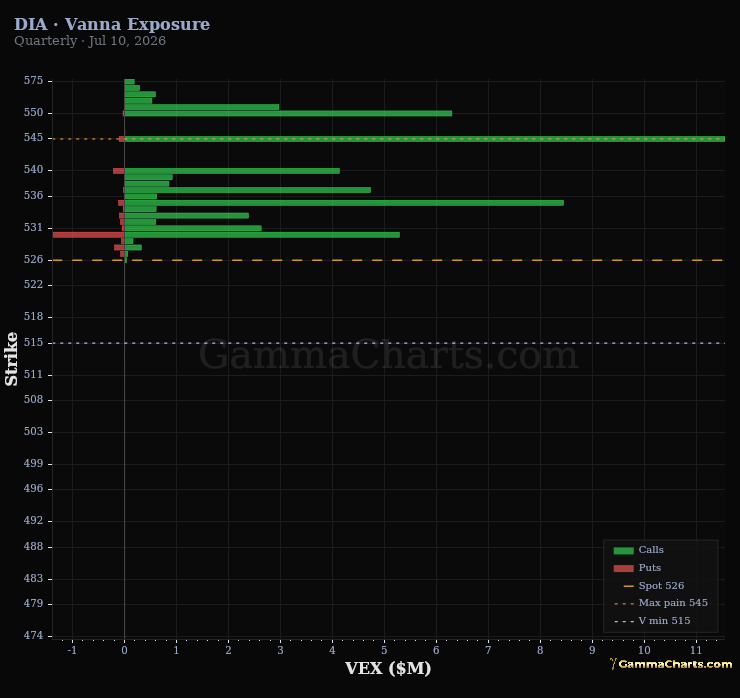

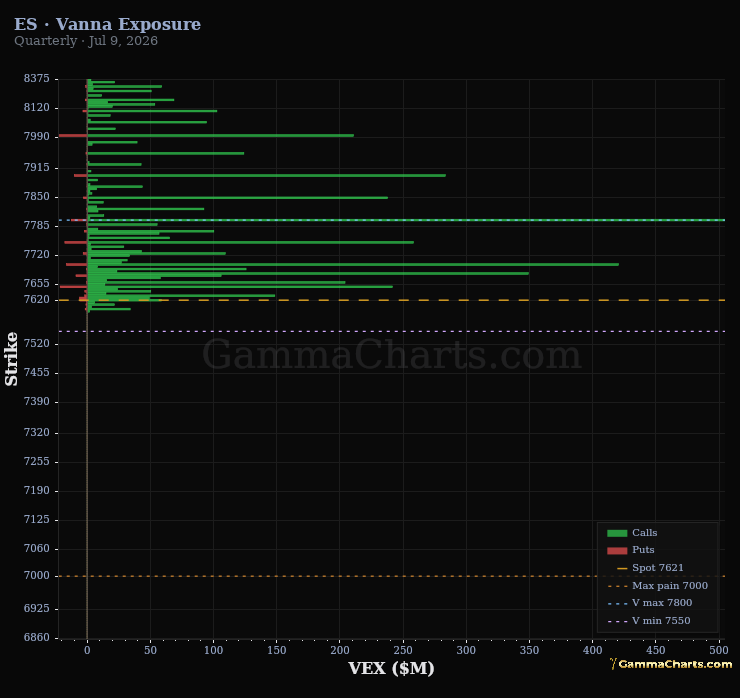

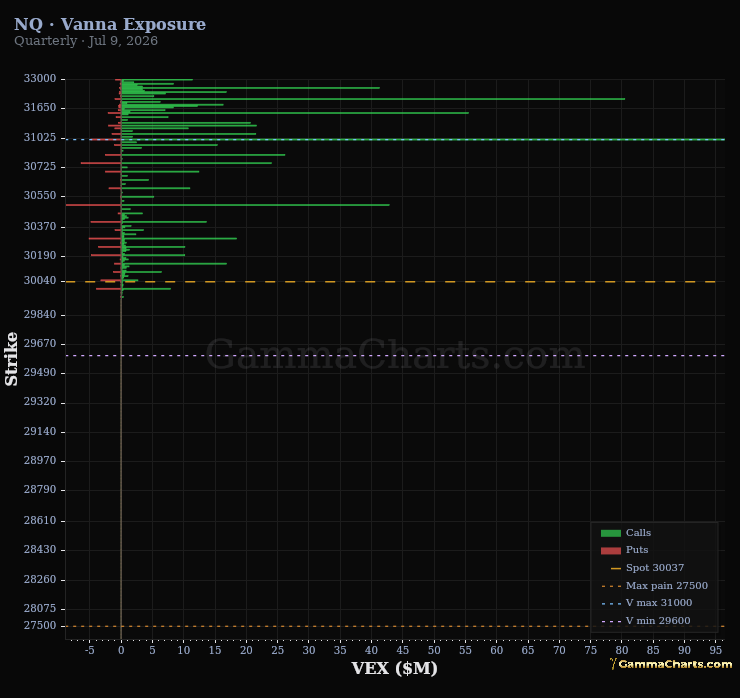

Vanna

Vanna is how much dealers must buy or sell volatility as spot moves. It explains why vol often rises when price falls — dealers are forced buyers of vol on the way down.

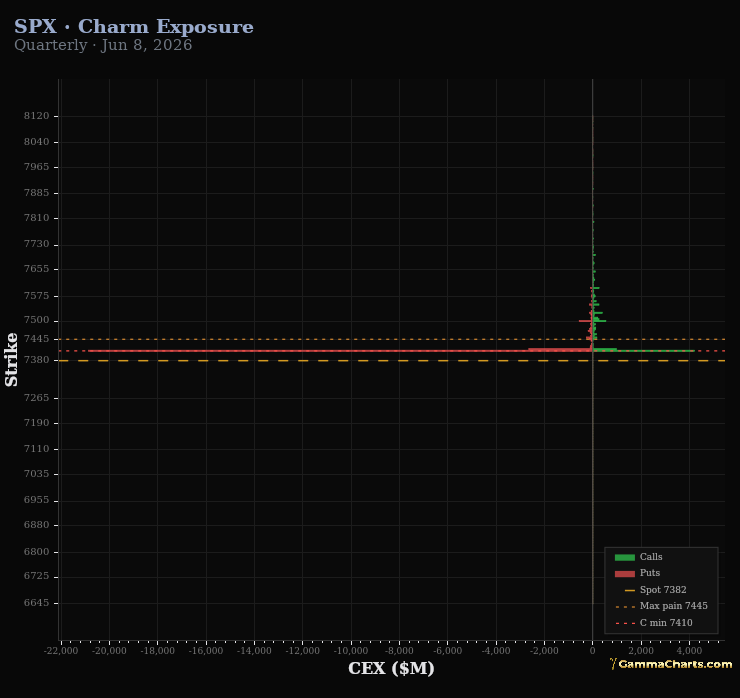

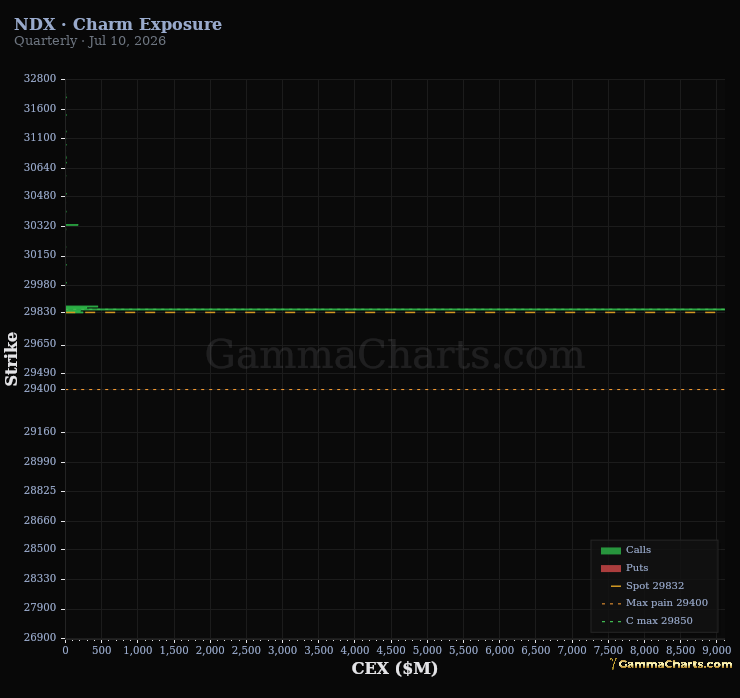

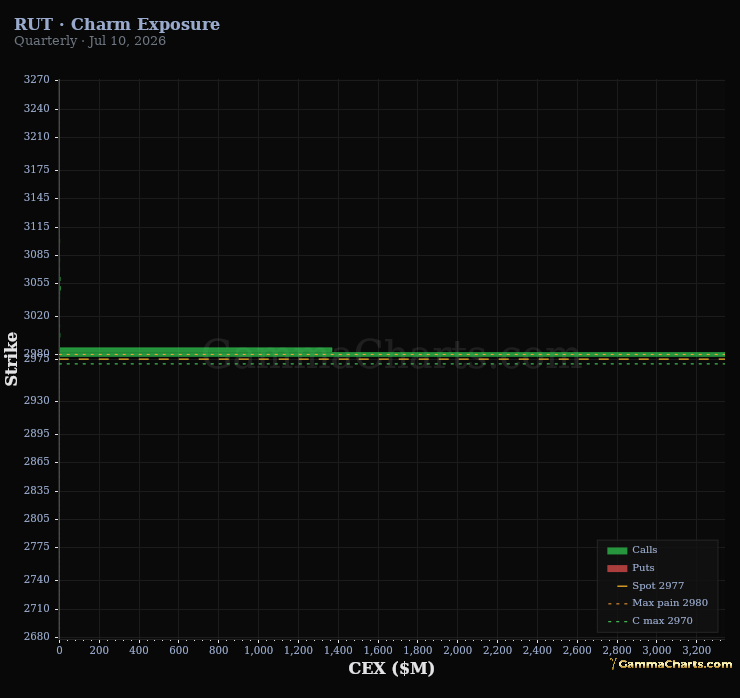

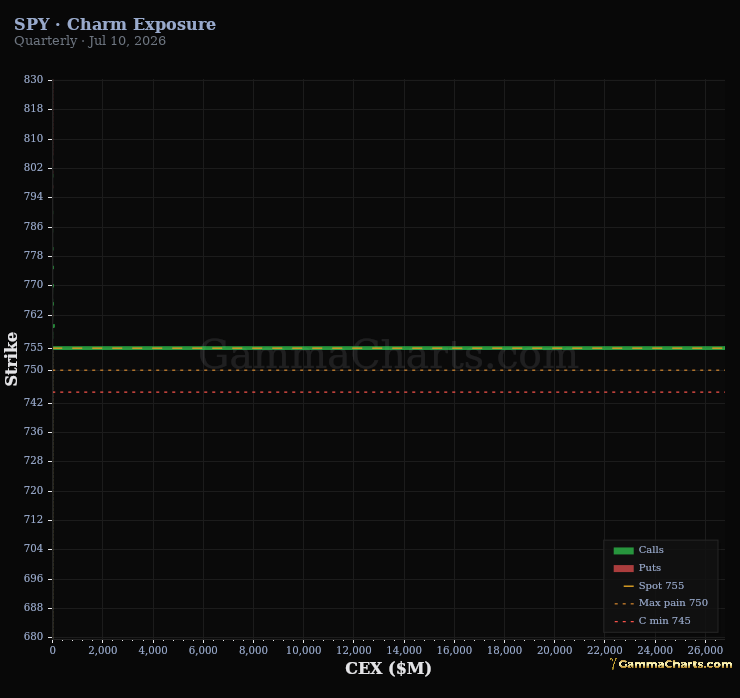

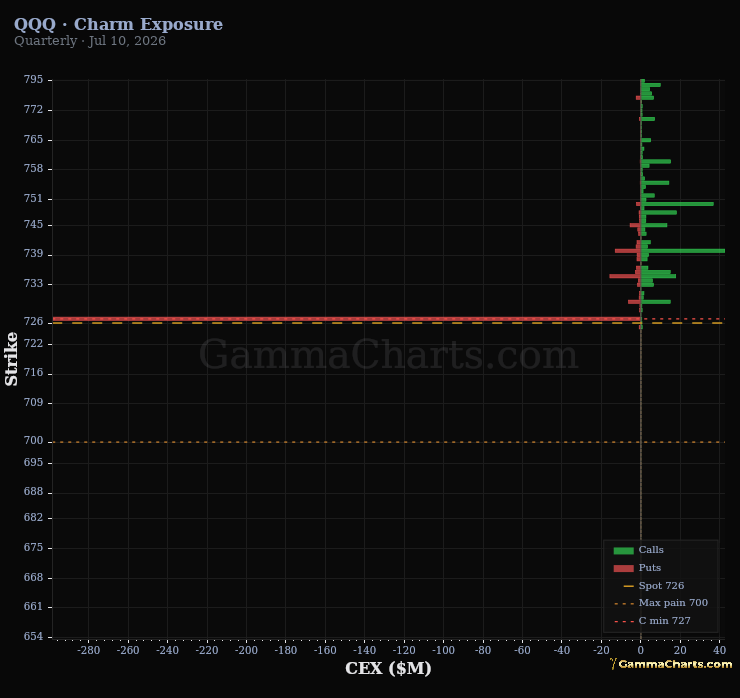

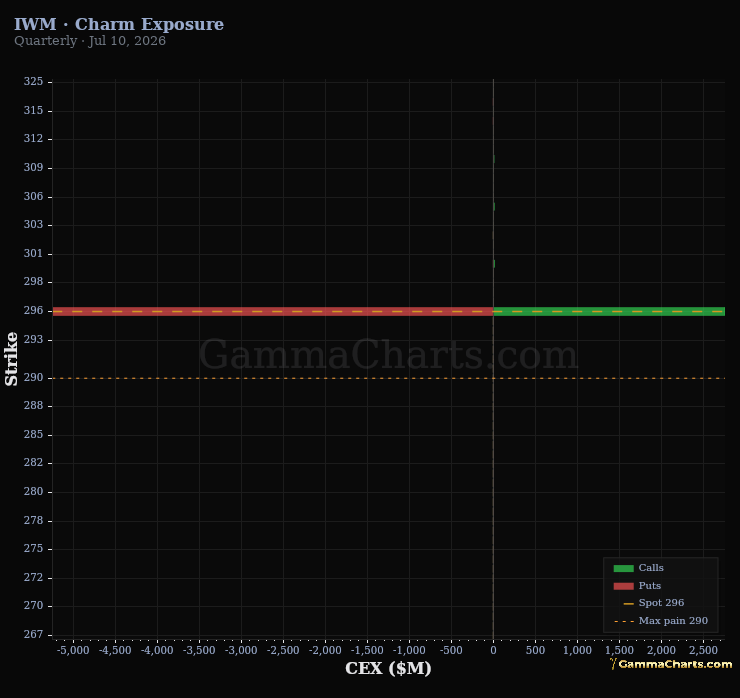

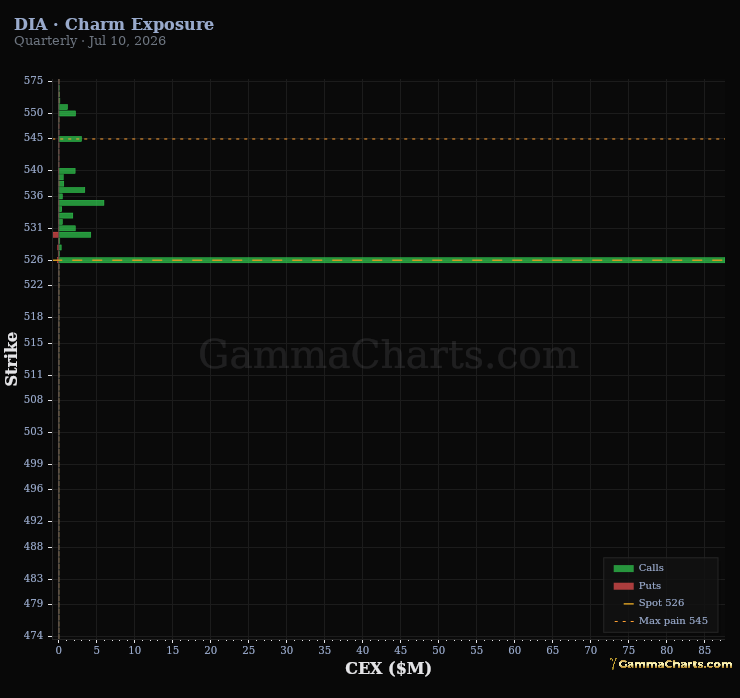

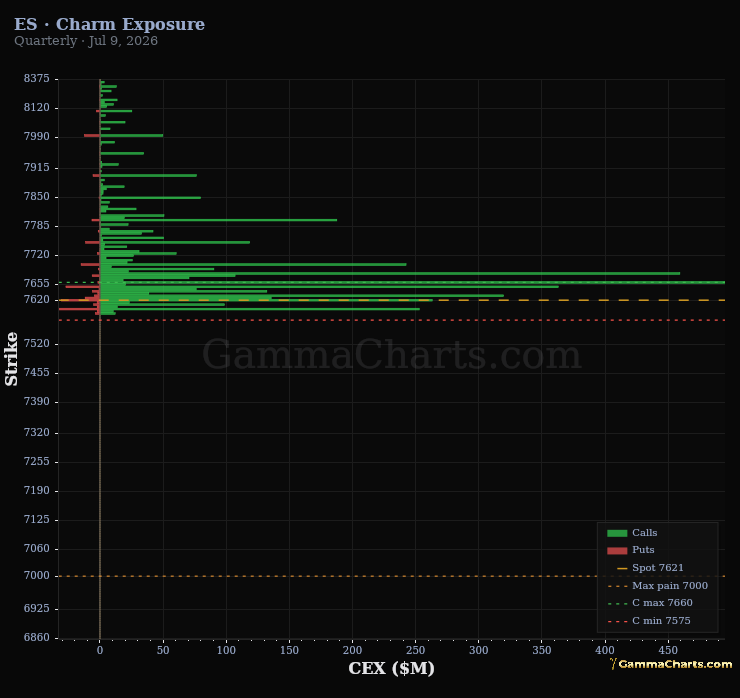

Charm

Charm is how much delta bleeds away with time. Dealers must unwind hedges as expiration approaches, creating predictable intraday flows.

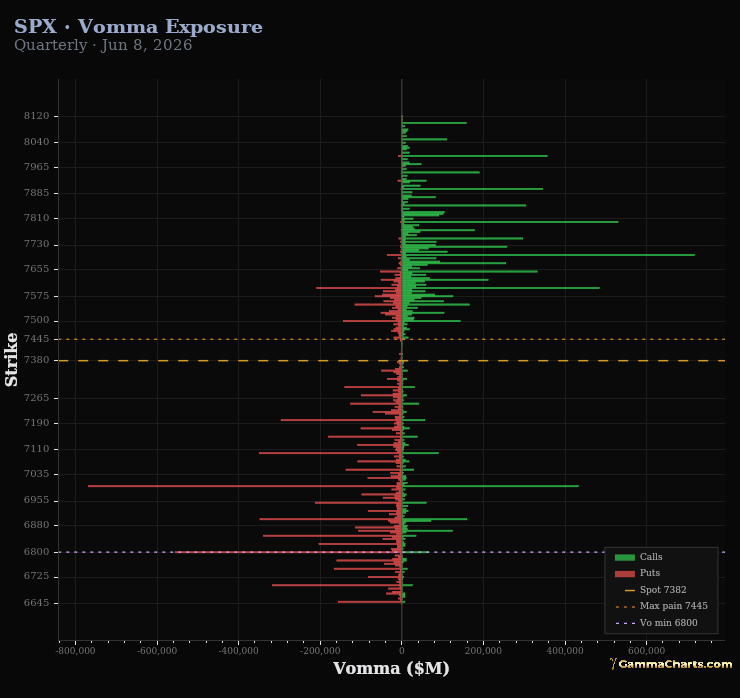

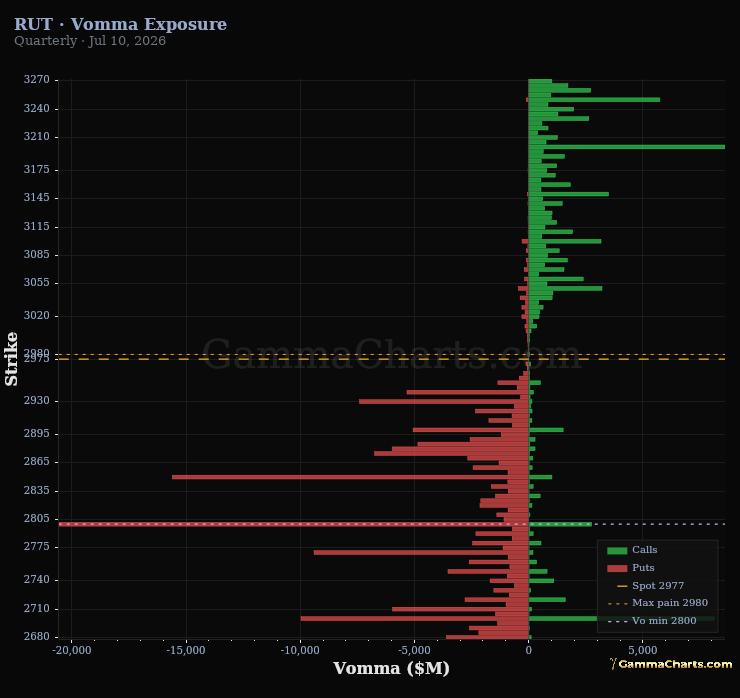

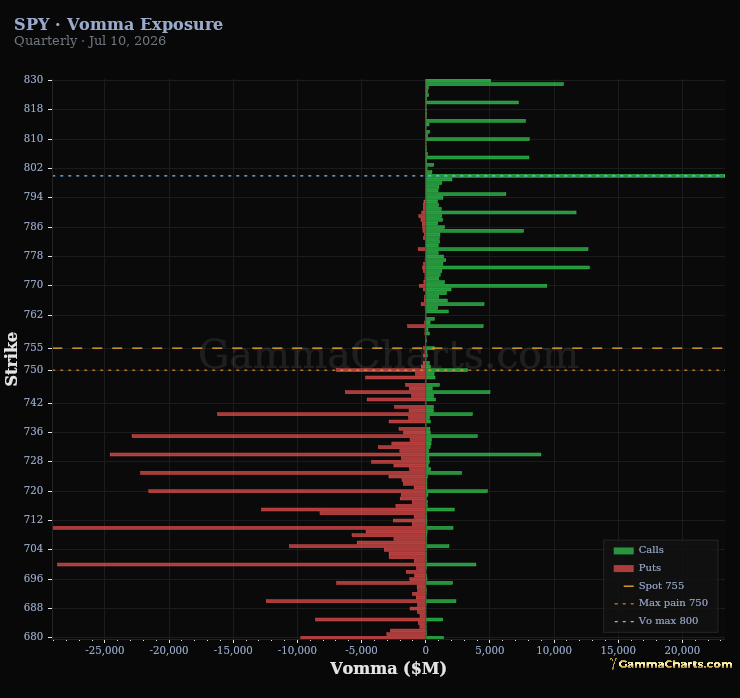

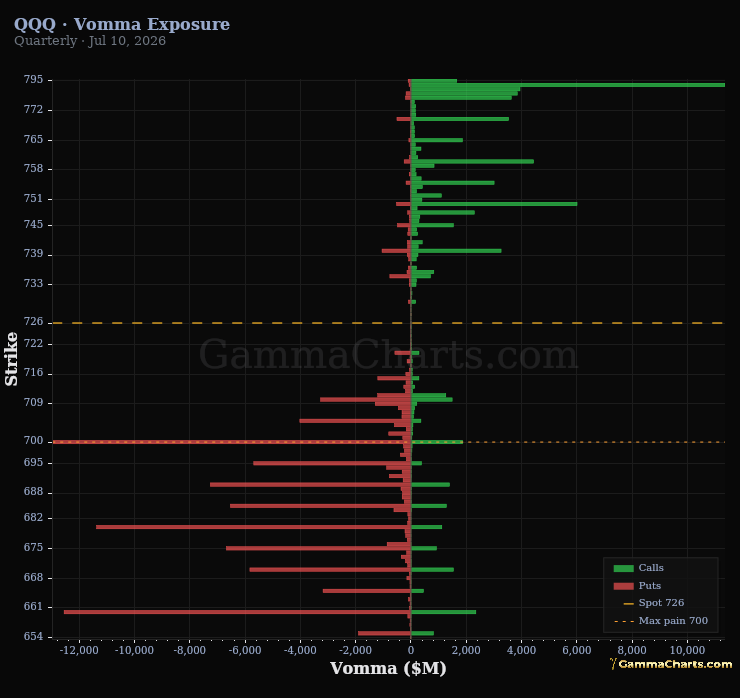

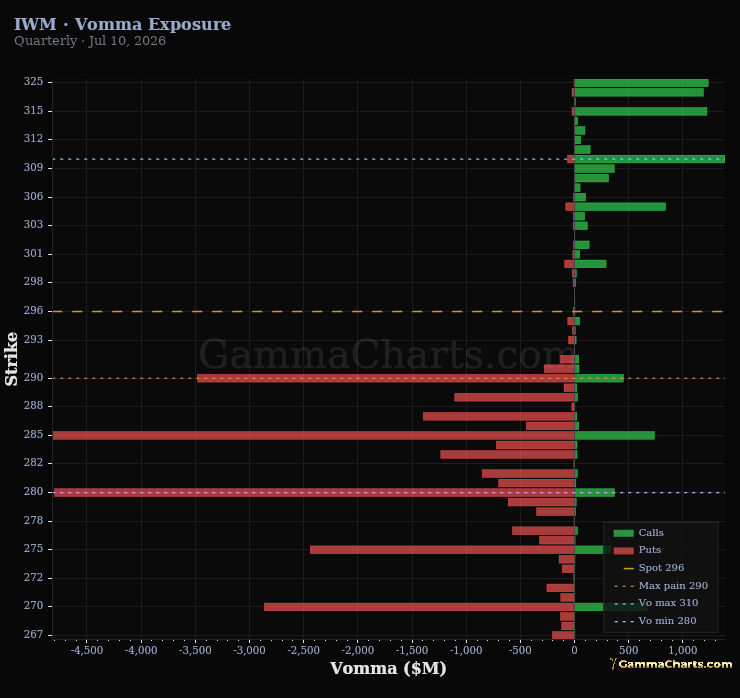

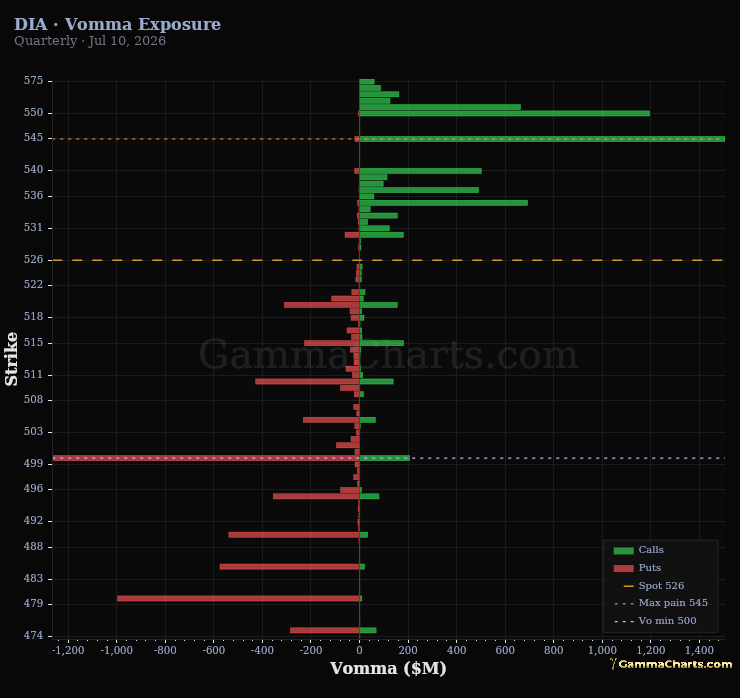

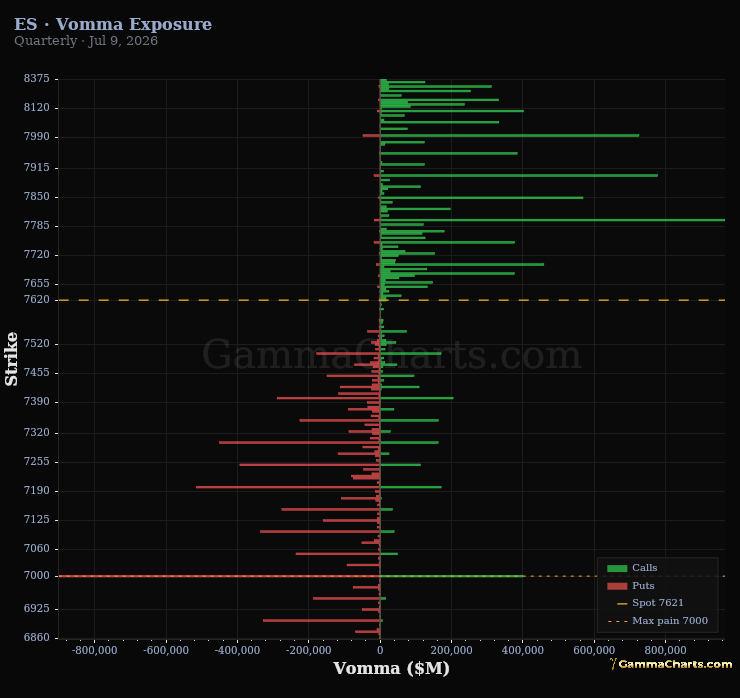

Vomma

Vomma is how much dealer vega changes as implied vol moves. High vomma means a vol spike forces additional vol hedging, accelerating the move.